As of March 2026, Minimum.com has been acquired by Novisto - cemeting Novisto’s position as the most comprehensive, "all-in-one" sustainability platform, designed to serve as the single source of truth for global enterprises navigating an increasingly complex regulatory landscape.

Minimum wrapped: 2025 in review

The one where: We look back over 2025. It’s been a tough year for corporate sustainability with diverging political and climate realities leading to a renewed focus on business value.

While there are signs of convergence in climate disclosure standards, the effectiveness of corporate climate governance remains in question. We unpack the year and look ahead to 2026.

A tough year for corporate sustainability

2025 has been a tough year for corporate sustainability. Global elections in 2024 returned largely climate-sceptic governments who wasted little time unpicking key elements of the corporate climate agenda.

While the strength of headwinds has varied - outright rollback in the United States, significant watering down in the EU, or a slowing of momentum in the UK - in aggregate, global climate ambition has been throttled for fear of alienating electorates and undermining competitiveness.

For those working in corporate sustainability this has made life challenging. Many sustainability teams are contending with a deprioritising of key climate initiatives, budget cuts, and increased scrutiny over how their role delivers business value.

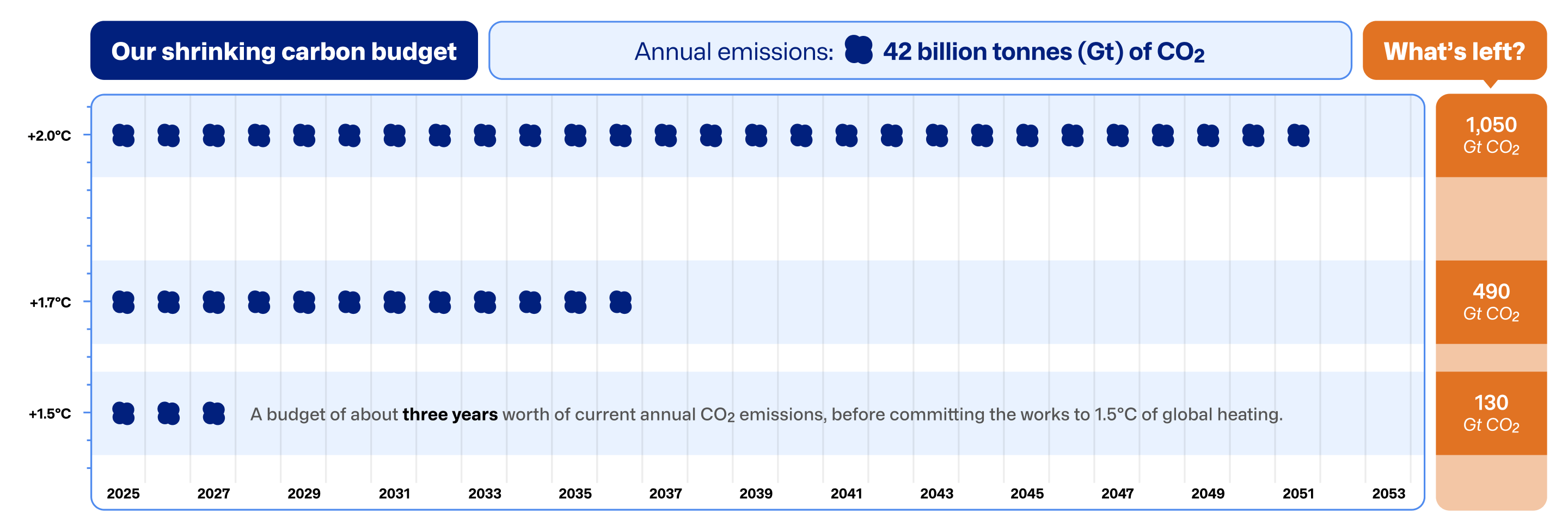

All the while, the climate crisis itself deepens. The latest UNEP Emissions Gap Report suggests that under current policies the world is on track to hit 2.8C of warming by 2100. A temperature rise that will have major implications for economic activity.

Fallback to financial materiality

But while the contrast between political and climate realities is stark, market forces remain more nuanced.

Multiple surveys point to external stakeholders retaining a strong appetite for understanding how companies are managing climate-related risks and opportunities. Whether that’s investors deciding whether to invest (and at what price), lenders setting the cost of capital, or customers deciding whether to do business with a company.

So while loftier corporate ambitions to make a positive difference have been substantially dialled back in 2025, climate data that makes businesses better at managing risks and improves profitability and cash flow still commands management and investor attention.

Increased consolidation and interoperability of climate standards

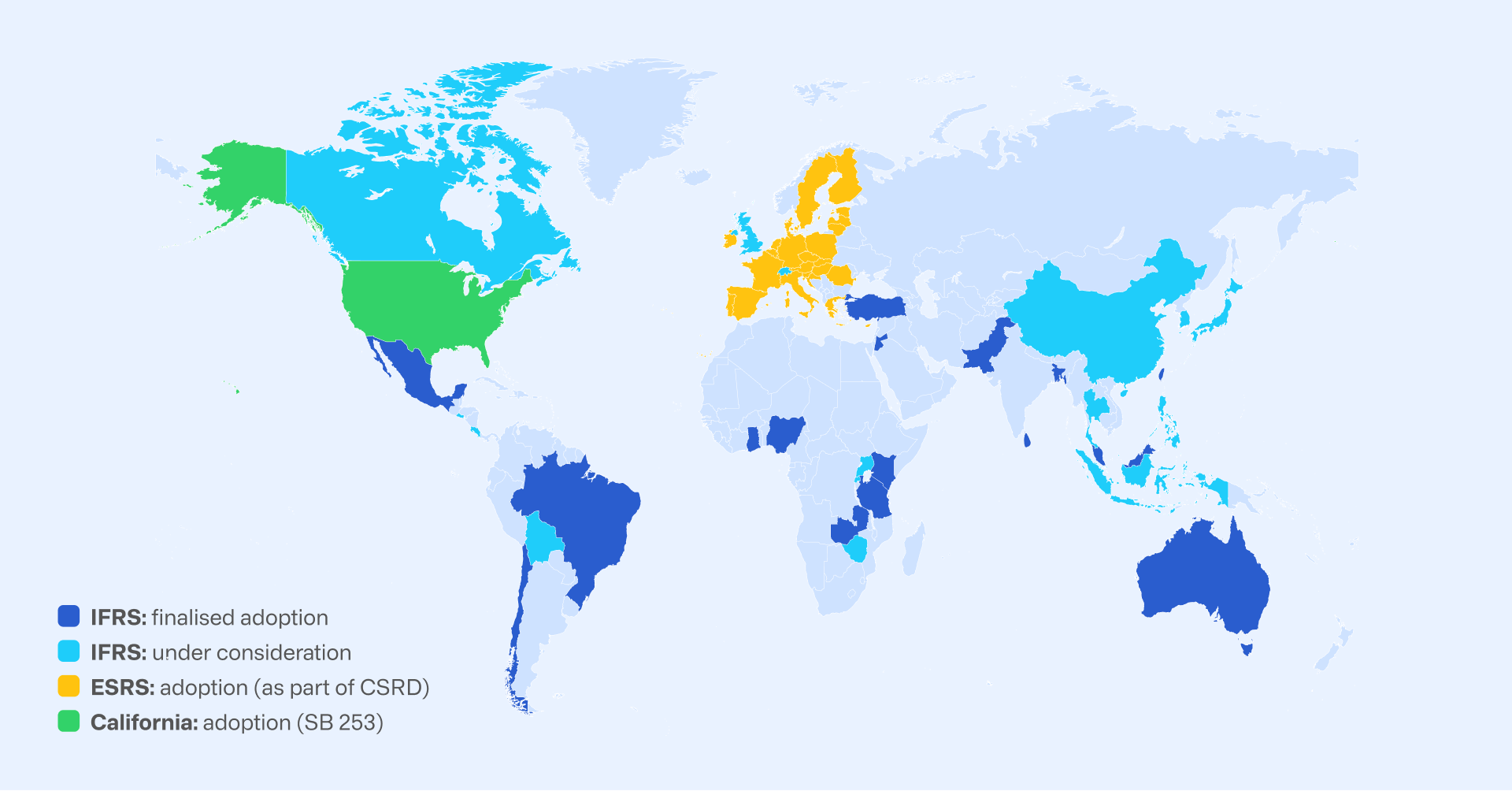

This explains why 2025 has seen positive progress in the adoption of the IFRS Sustainability Disclosure Standards (IFRS SDS). The SDS were designed to be a “global baseline” for sustainability disclosures to meet the information needs of investors interested in how climate change could impact the businesses they’re investing in. This financial materiality focus is distinct from measuring how the business itself impacts the environment.

The IFRS sustainability standards are now in the process of being adopted by around 40 jurisdictions representing close to 60% of global GDP, though they are not always mandatory. Where the EU had once intended to go further, simplified European Sustainability Reporting Standards (ESRS) released earlier this month have moved much closer to the IFRS baseline.

Emissions standards are also aligning. In September, the GHG Protocol and ISO announced a strategic partnership to harmonise greenhouse gas standards and co-develop new standards.

Climate governance in question

But greater alignment on disclosure has not resolved deeper questions about whether current climate governance is actually driving change.

To date, the focus has primarily been on encouraging companies to set, disclose and deliver on emissions reduction targets as a way of aligning corporate climate action with global efforts to reduce emissions in line with 1.5C.

Yet, as we discussed in our July newsletter, it’s increasingly unclear whether this is delivering meaningful changes in companies’ business models that address their most critical emissions sources.

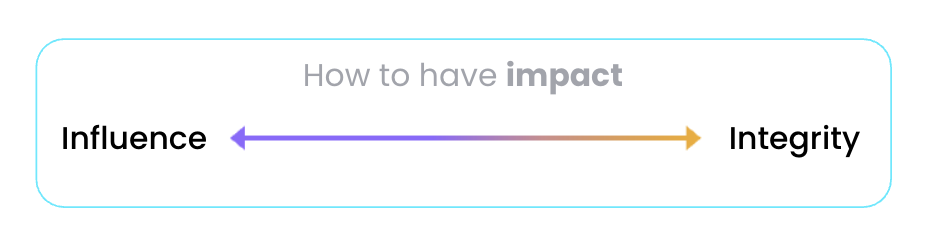

Impact vs. integrity

At the heart of the debate is a fundamental design problem: finding a way to create incentives for companies to take climate action (and receive credit for doing so), while at the same time ensuring such action is meaningful and high integrity.

This tension is apparent in the GHG Protocol’s ongoing revision of its corporate suite of standards - a topic we explored in depth this year, including in a recent webinar. For example:

- The GHG Protocol’s current consultation is seeking feedback on proposals to both tighten Scope 2 Guidance and allow possible use of impact accounting methods.

The proposed revisions to the Scope 2 Guidance focus on introducing hourly matching for purchased renewable electricity. This is mainly designed to inject more integrity into firms’ scope 2 market-based claims.

Meanwhile, giving more prominence to impact accounting would furnish companies with additional ways to report on a wider array of mitigation actions that may not be captured by traditional inventory reporting. Impact accounting has influential advocates as well as detractors who fear a muddling of corporate climate achievements.

- On the scope 3 side, poor data quality remains a limiting factor preventing companies from taking greater action to address value chain emissions. This is a key consideration behind draft GHG Protocol proposals to require firms to disclose more detail on the specificity of their scope 3 data.

- But there is also growing recognition that emissions targets may need to be complemented by a broader assessment of necessary sector-specific transitions. The SBTi’s recent proposals for updating its Corporate Net Zero Standard partly incorporate this perspective.

What’s ahead for sustainability teams in 2026?

Taken together, the political shifts, standards convergence, and governance debates of 2025 made for a year in which climate and political realities drifted apart. Focusing on financial materiality will likely be the best option for most sustainability teams to bridge climate and business realities in 2026.

As we highlighted in last month’s webinar, now more than ever sustainability needs to be framed in ways that resonate with how executives allocate capital. If sustainability is presented as an overhead - rather than as a driver of revenue, cost reduction or competitive advantage - in today’s environment it will lose in the boardroom.

Unlocking business value is not simply about having data that seems good enough for disclosure. This might tick the box with investors (for a while). But it won’t be sufficient to actually manage the underlying issues required to deliver business value and showcase impact (see our White Paper for a more detailed discussion).

Getting ROI from technology

In this regard, technology can help companies deliver both business value and sustainability objectives - but only where the return on investment (ROI) is clear.

Looking ahead to 2026, the strongest ROI will come from software that delivers in two areas:

- Automate emissions calculations: the right software can significantly reduce the time and resource spent calculating emissions, unlocking efficiency savings that resonate with the C-suite. This has long been promised, but the technology is now mature enough to deliver real results - more frequent footprints with fewer manual errors - bringing sustainability data closer to financial data for day-to-day management.

- Deliver better data quality: most software tools can produce attractive dashboards and automate reporting, but data quality is what ultimately matters. Software that enables the collection of highly specific activity data and emission factors, and optimises hybrid footprint calculations, delivers outputs that are actionable and ready for evolving climate governance.

The Minimum Line

Thanks to everyone who has read our newsletters and attended our webinars this year. There will be more to come in 2026. In the meantime, on behalf of the whole team at Minimum, we wish you a restful end to the year.