As of March 2026, Minimum.com has been acquired by Novisto - cemeting Novisto’s position as the most comprehensive, "all-in-one" sustainability platform, designed to serve as the single source of truth for global enterprises navigating an increasingly complex regulatory landscape.

Scope 2 Gets Serious: Hourly Matching and Greater Precision

We look at proposed changes to scope 2 location- and market-based reporting. Back in February and May we outlined where scope 2 might be heading. The latest proposals confirm much of that direction and sharpen the picture with a focus on greater precision and hourly matching.

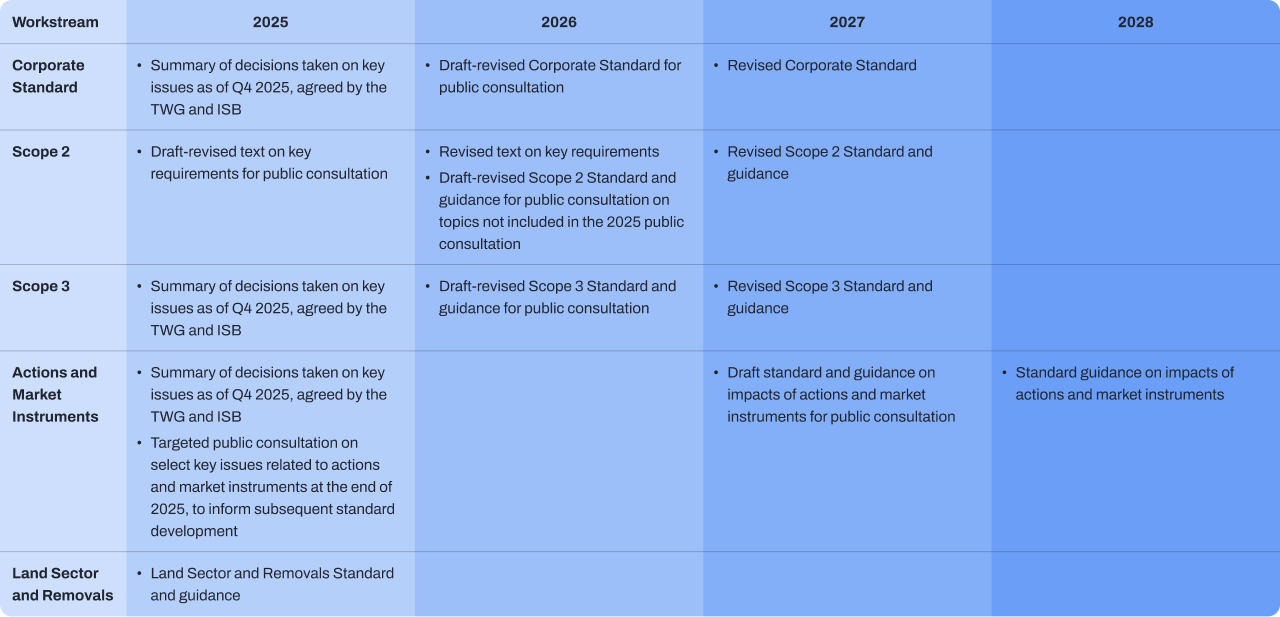

Last month the GHG Protocol’s Independent Standards Board (ISB) signed off on the first wave of proposed changes to its suite of corporate standards. This month we focus on the updates to the scope 2 standard, which are set for public consultation in the autumn.

Slow and steady wins the race

The revision of the corporate suite of standards is progressing slowly. It began in 2022 with a series of public consultations that set the agenda for technical working group discussions.

Over the past year, those working groups met regularly to debate possible changes, culminating last month in a first set of proposals presented to the ISB for feedback and approval.

These proposals will form the basis of exposure drafts for public consultation next year. And, in the case of scope 2, an initial consultation this autumn.

The GHG Protocol intends to publish final revised standards in 2027, likely as a single consolidated document. A further phase-in period would seem reasonable to allow companies to adjust, meaning the final impact might not take effect until the latter part of the decade.

The slow process reflects both the breadth of the revision and the high stakes of getting it right. With more companies now subject to mandatory disclosure, the standards are under mounting scrutiny to ensure comparability and transparency, while creating incentives for climate action.

The GHG Protocol needs to strike a balance between pressures to enhance comparability (more granular and specific standards), while ensuring completeness (retaining some flexibility and breadth). As well as find ways to facilitate companies having greater climate impact at the same time as safeguarding the integrity of climate claims.

The scope 2 challenge

As we outlined in our February newsletter, scope 2 is a clear example of the balancing act facing the GHG Protocol.

On the surface it looks like a bright spot in corporate decarbonisation. But dig deeper and the picture gets murkier: measurement approaches are often unrepresentative, companies’ interventions (such as renewable electricity procurement) vary widely, and there are doubts about the real impact of certain instruments, like renewable energy credits (RECs).

As we noted in May, the GHG Protocol’s main focus has been on improving the precision and accuracy of the two main reporting methods:

- Location-based method, which reflects the average emissions intensity of electricity grids where consumption takes place, and

- Market-based method, which reflects emissions from generated electricity that companies have purposefully chosen to buy.

It has also been debating whether to require or recommend that companies report on the emissions impacts of their actions in the electricity sector.

The latest feedback from the Independent Standards Board now provides a clearer picture of the way forward, which we expect to see reflected in the consultation.

Location-based proposals

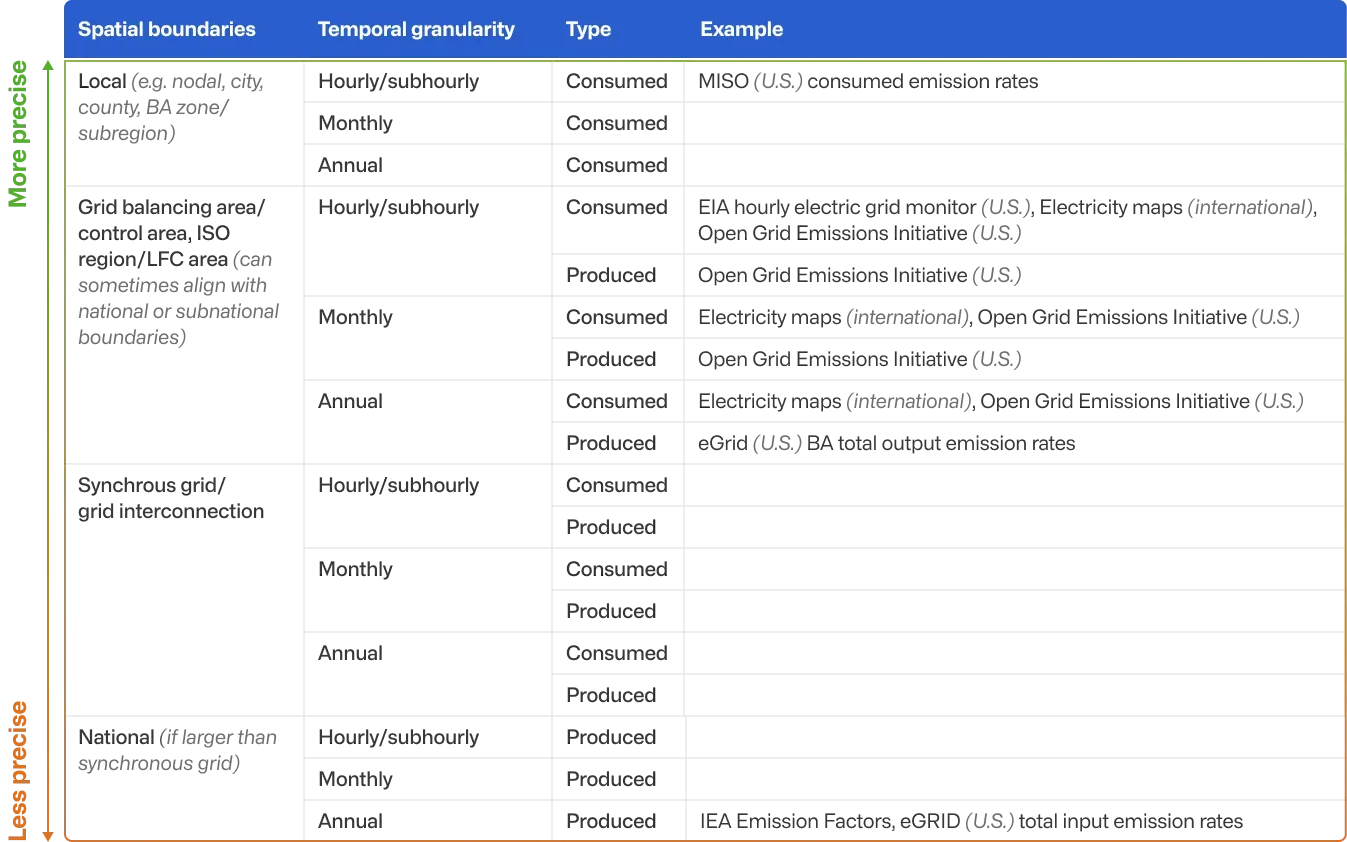

The new proposals would require companies to use more precise emission factors, provided they are “accessible” and align with underlying activity data.

The aim is to give companies a more accurate picture of the emissions associated with the electricity they consume from the grid, helping them identify transition risks and shape abatement plans. For many firms, this will mean sourcing more granular grid data than they currently use and building systems to handle higher-frequency reporting.

The revision will require firms to use emission factors that are:

- Spatially specific: as close as possible to the grid where consumption occurs, instead of national-level factors

- Temporally granular: aligned as closely as possible with the hour of consumption, rather than monthly or annual averages

- Consumption focused: based on consumption, rather than production, which can be distorted by imports and storage discharge.

The table below illustrates the proposed hierarchy:

To ensure feasibility, the choice of emission factors will be subject to two additional criteria:

- Accessibility: emission factors must be publicly available, free to use, and from a credible source. The ISB has asked the GHG Protocol to more tightly define these terms, but it’s safe to say that firms won’t be obliged to buy more specific emission factors from private providers (though they may elect to do so).

- Reflective of available activity data: for example, if a company only has monthly or annual activity data, it would not be required to report hourly even if hourly emission factors exist (though it could opt to use estimated hourly data).

It is important to emphasise that for location-based reporting companies are not required to match hourly consumption with renewable or zero-carbon energy, only to report on a timelier basis when the data is available.

Market-based proposals

The market-based proposals would tighten requirements on the contractual instruments companies use to match electricity generation to their consumption, introducing new criteria for hourly matching and deliverability.

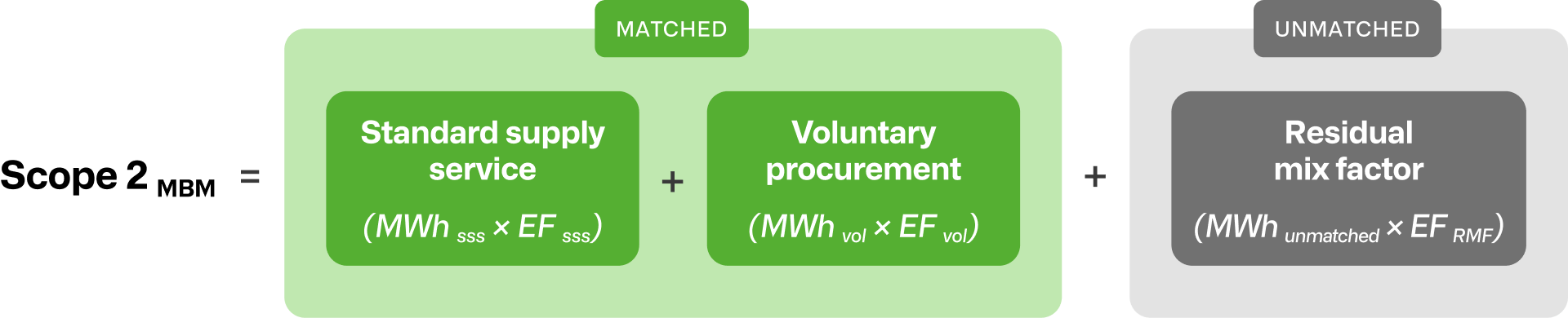

As we outlined in May, companies will need to separate the share of electricity they match to generation sources into:

- Standard Supply Service, a new concept designed to ensure fair and proportionate claims for shared, regulated, or publicly funded generation. Companies would be allocated a fair share of this generation to prevent inflated claims.

- Voluntary Procurement, where a company can demonstrate exclusive financial and contractual ownership over a generation source. This includes contract-based renewable energy purchases like PPAs, as well as RECs.

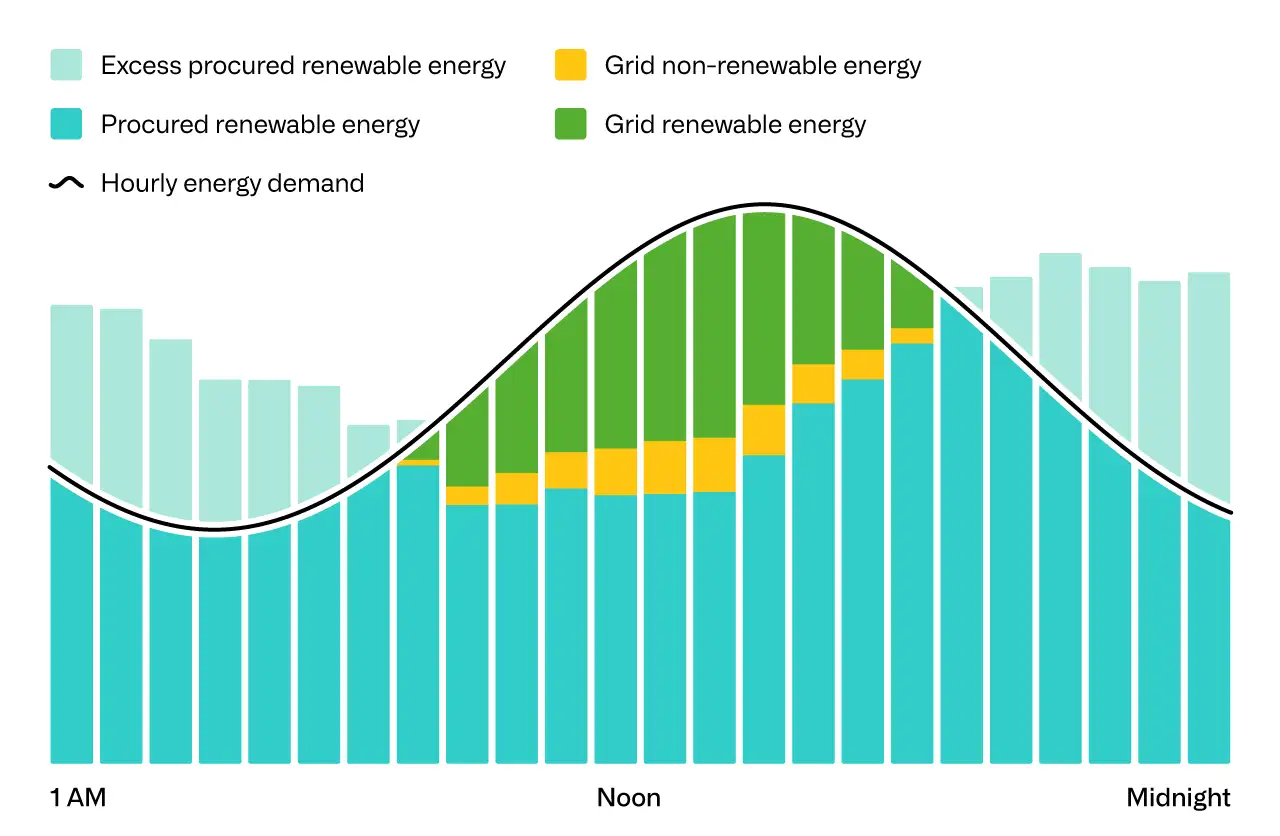

Certain companies would also face new hourly matching requirements - meaning contractual instruments (e.g. RECs) must be matched with electricity generated in the same hour as the electricity consumed by the company. This would be a step change from current arrangements which allow for matching at any time within the same calendar year.

The intention is to capture differences between when a company might consume electricity (e.g. at night) and when renewable energy is available (think solar power), creating incentives for firms to invest in new technologies (e.g. storage) or proactively shift loads.

In practice, this could reshape how companies procure renewable power with direct consequences for contract strategy, risk management, and energy costs. Introducing additional constraints to the supply of RECs would likely increase prices for hourly RECs during hours when renewable energy is scarce, increasing the financial subsidy and incentives towards development of new technologies that may currently be uncompetitive.

Given that the hourly matching requirements will be challenging for many companies to operationalise, the GHG Protocol is likely to consult on options to ease implementation, such as:

- Introducing a load-based threshold - so only the largest, most energy intensive companies are required to undertake hourly matching. A threshold does not appear to have been agreed yet - and will likely be subject of consultation - but the working group has contemplated figures such as total annual electricity consumption of 10 GWh per year.

- The GHG Protocol is also considering a volumetric threshold which would exclude a certain percentage (5-10%) of total electricity from hourly matching requirements.

- Grandfathering existing contracts - allowing long-term contracts signed before the update to retain eligibility.

- Allowing estimated hourly profile data to represent how electricity is used or generated over time when direct hourly measurements aren’t available.

- A long phase-in period to allow companies to adapt.

The new market-based rules would also require companies to meet deliverability requirements, meaning contractual instruments must come from the same market in which the companies’ electricity-consuming operations are located. The objective is to prevent firms from procuring energy that can’t actually be dispatched in the relevant grid.

This would mean generation must happen in a market with a physical interconnection or coordinated market operations linked to the grid where consumption occurs. Limited exemptions may be allowed where a company can demonstrate physical delivery from the point of generation to consumption, or clear evidence of excess transmission capacity in the generating market.

In its feedback, the ISB asked the GHG Protocol to provide more detail on aspects such as the use of profiled loads for hourly matching, potential exemptions, deliverability rules, and the treatment of Standard Supply Service.

Finally, the ISB has decided to pause the working group’s current activity on developing a project-based impact accounting approach for scope 2 (see our May newsletter). This will instead be picked up by the separate Actions and Market Instruments group, which is moving at a slower pace.

The Minimum Line

Hourly matching is shaping up to be a key flashpoint in the scope 2 revision. Indeed, it would represent a significant change for energy-intensive companies who are currently permitted to make renewable energy claims based on certificates from energy generated at any time during the same calendar year and with relatively broad market boundaries.

Proponents argue that it would strengthen credibility in corporate claims and create better price signals that could spur the development of storage and flexible clean power technologies. They see it as the logical next step toward a more accountable system.

Critics counter that it could risk making PPAs less attractive and REC procurement more complex and costly. They warn it could reduce participation in voluntary markets and ultimately slow the pace of renewable development.

For companies, the stakes are high: if these rules are approved, procurement and reporting strategies will need a fundamental rethink. The consultation is the moment to weigh in. It’s also the time to start evaluating whether current systems, contracts, and data flows are ready for what may lie ahead.