As of March 2026, Minimum.com has been acquired by Novisto - cemeting Novisto’s position as the most comprehensive, "all-in-one" sustainability platform, designed to serve as the single source of truth for global enterprises navigating an increasingly complex regulatory landscape.

Widening The Lens Of Corporate Climate Impact

We take a look at a new initiative - the Task Force for Corporate Action Transparency - offering companies more options to claim credit for their climate mitigation action. A useful way to incentivise action, or a smokescreen for less substantive progress?

Widening the lens of corporate climate impact

The Task Force for Corporate Action Transparency (TCAT) was launched last month with the goal of addressing perceived gaps in current guidance on climate mitigation reporting.

TCAT advocates broadening the lens of existing inventory-based accounting to allow for complementary impact-based reporting. The goal is to provide companies with more ways to report on a wider array of mitigation actions that may not be captured by current reporting.

Indeed, critics have long argued that existing standards (GHG Protocol, SBTi) inhibit companies from reporting (and taking credit for) a full range of climate actions, including impacts obtained outside their inventory, interventions where the physical connection to the emissions source is indirect or purely financial, or efforts to facilitate the uptake of new technologies.

While these complaints are not new, the emergence of TCAT warrants closer attention.

Firstly, because the group has already put together two well-constructed guidance documents on Mitigation Action and Targets, developed by recognised GHG accounting experts. It’s also backed by influential corporate sponsors (Pepsi, Netflix, Etsy, Amazon) and endorsed by several non-profit organisations (mostly from the voluntary carbon markets - a message in itself).

It’s also timely. The GHG Protocol has begun to explore some of these issues as part of work on a new Actions and Market Instruments standard or guidance. But technical working group discussions appear to have faltered, creating an opportunity for TCAT to set the agenda.

Inventory vs. impact accounting

At the heart of TCAT’s proposals is increasing the visibility of impact accounting as a way to report a wider range of real-world impacts from corporate climate action.

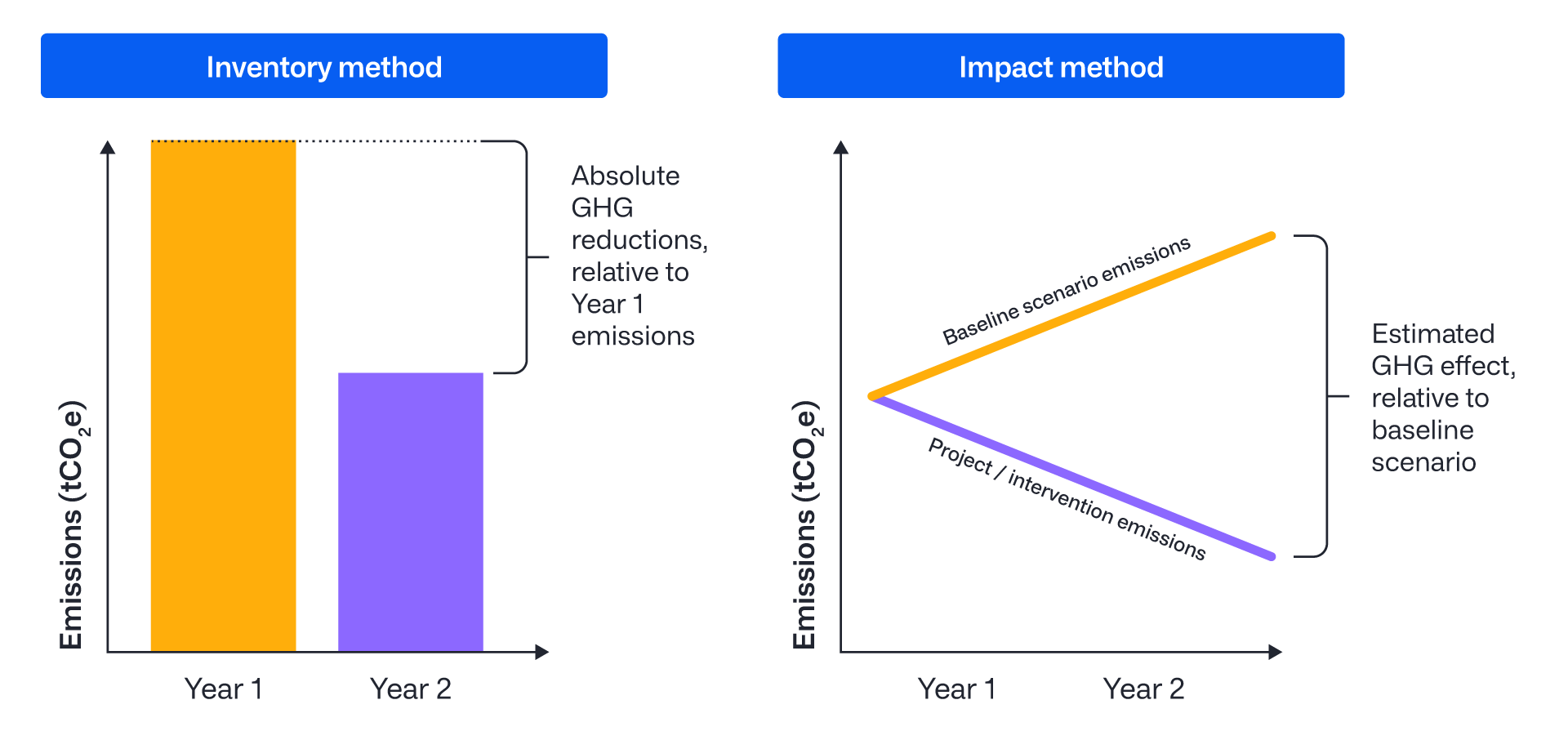

Current GHG Protocol standards are based on a separation between inventory (the Corporate Standards) and impact accounting (such as the Project Accounting Standard).

Most companies are familiar with and used to applying inventory accounting, reporting their absolute company-wide operational and value chain emissions for comparison over time.

By contrast, impact accounting is used to measure and report GHG emissions reductions or increases associated with specific activities relative to a counterfactual baseline scenario.

Avoided emissions are an example: they reflect the difference between emissions that occur due to a company's actions (e.g. its solutions and products) and the emissions that would have occurred without the solution.

Impact accounting is also used for carbon credits, which buy emission reductions or removals outside a firm's value chain and are sometimes claimed by companies to offset their own inventory emissions - blurring the two approaches.

The problem with impact accounting is the counterfactual - we simply can’t know what might otherwise have happened which creates a temptation to overstate.

Towards a multi-statement reporting approach

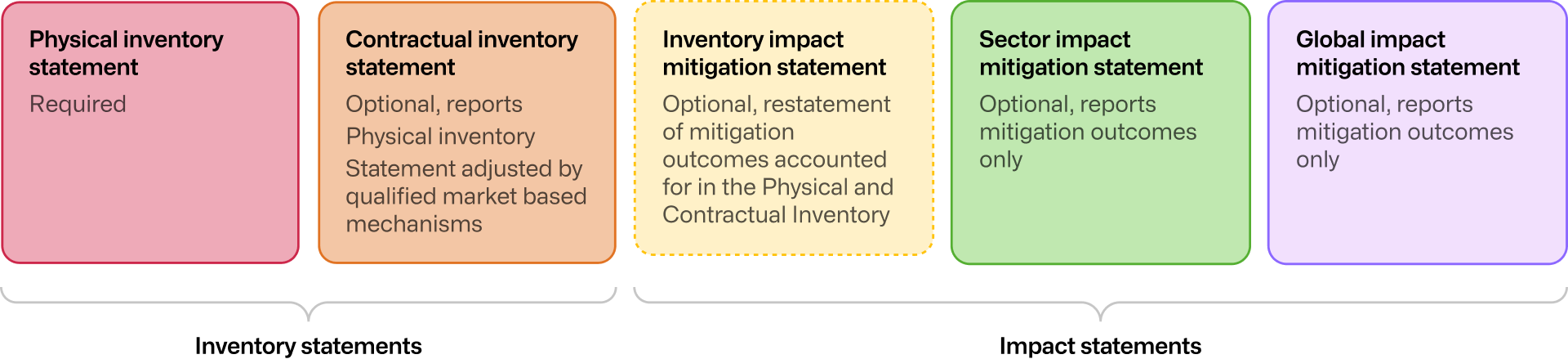

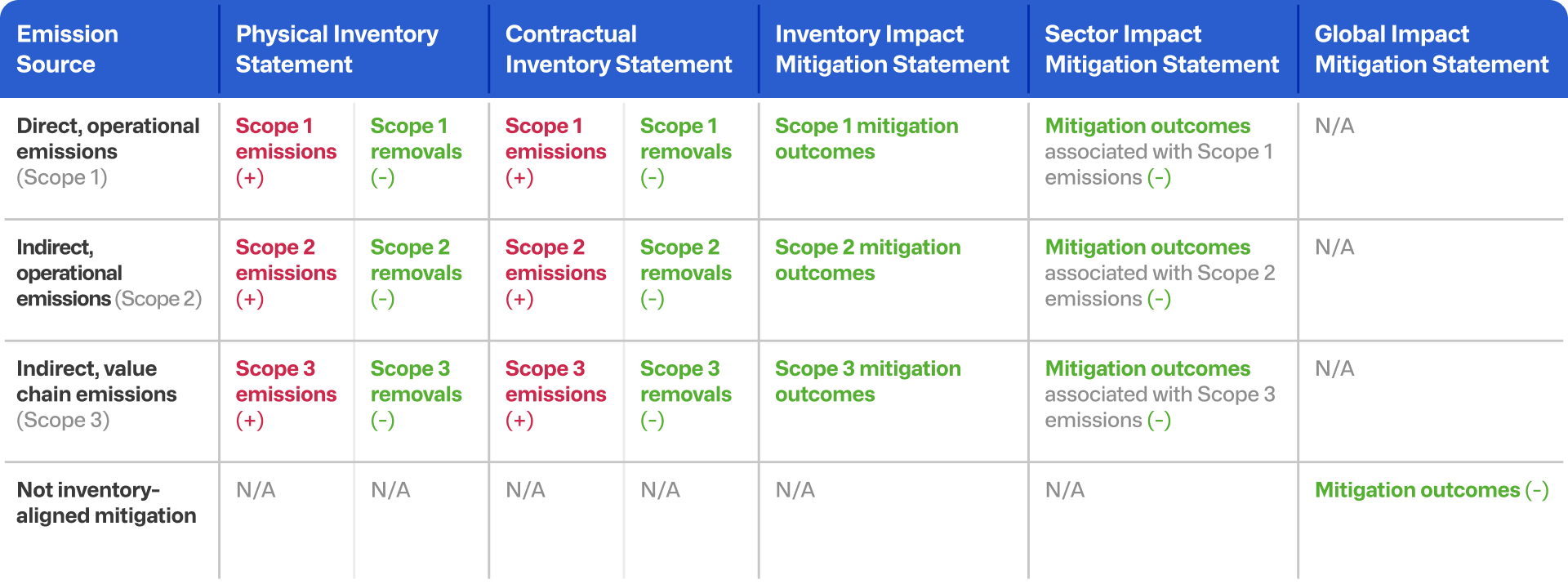

The Task Force proposes that companies should report their corporate climate impact using a multi-statement reporting framework. This would consist of five different reporting statements formed of inventory and impact reporting approaches.

All statements would be optional except for a Physical Inventory Statement. But the idea is to provide companies with the tools to report on activities that might have an emissions impact but may not currently be captured by inventory reporting.

Inventory statements

For “traditional” inventory reporting, TCAT guidance steers relatively close to the existing GHG Protocol suite of corporate standards albeit with a crucial difference.

Companies would be required to disclose a Physical Inventory Statement, reflecting the emissions associated with physical products, goods or services that the firm purchases or uses. This is essentially the same as under existing GHG Protocol rules, except contractual instruments used for market-based Scope 2 reporting would not be captured in this statement.

Instead, any contractual instruments that a company acquires (e.g. renewable energy credits or Sustainable Aviation Fuel certificates) may optionally be reported in a separate Contractual Inventory Statement which would reflect these adjustments.

Unlike GHG Protocol guidance, which focuses solely on scope 2, this statement would allow companies to report market-based emissions across all scopes. For example, if a company buys Sustainable Aviation Fuel certificates, these could potentially be used to report market-based scope 3 business travel emissions.

Impact statements

For climate action that might not be fully captured by inventory accounting, TCAT proposes that companies should have the option to report on such outcomes using impact accounting.

Companies would be able to choose between one of three impact statements depending on whether the outcome relates to:

- Decarbonising a firm’s own inventory: captured in an Inventory Impact Mitigation Statement.

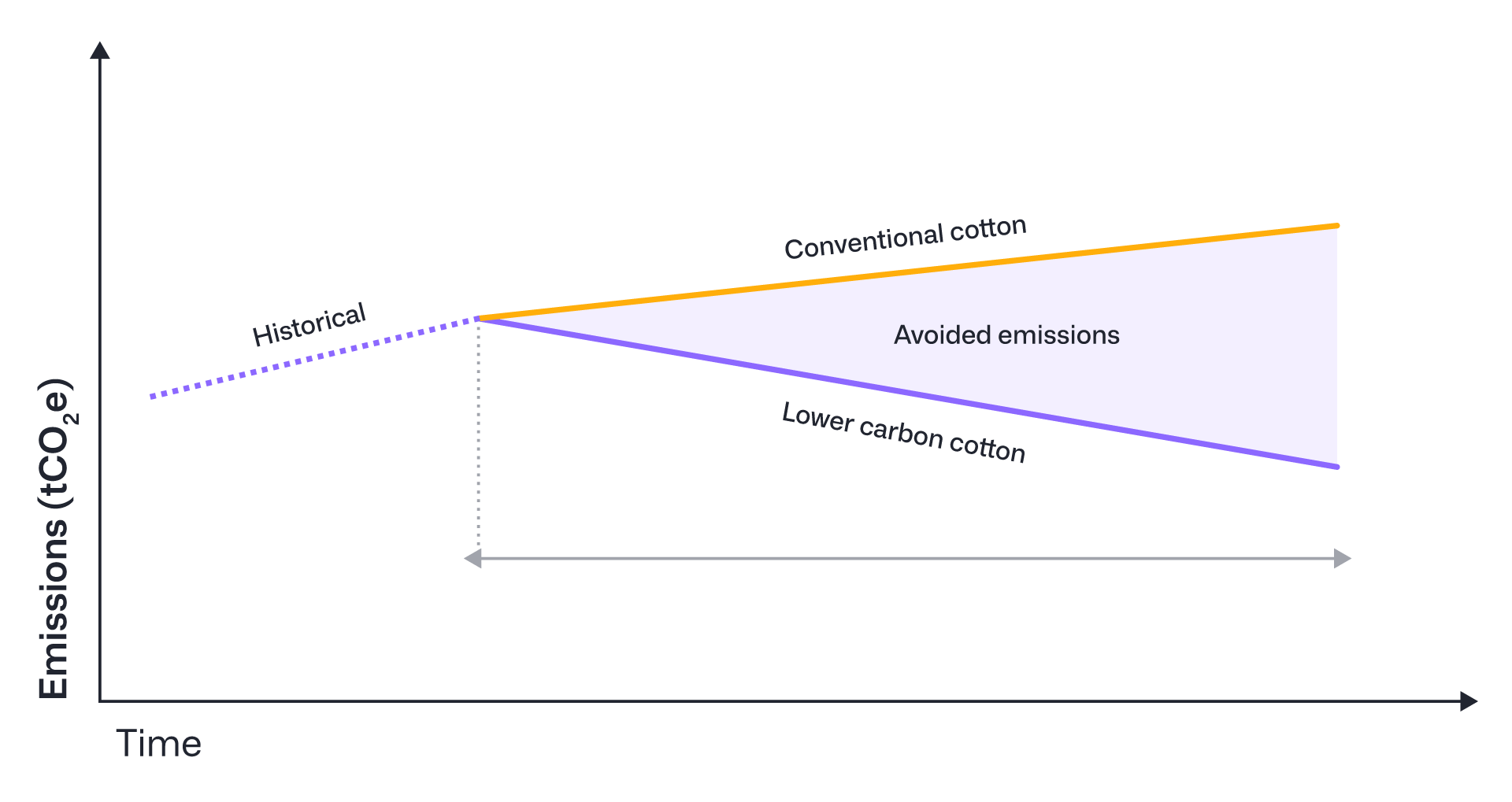

For example, an apparel manufacturer using cotton could decide to switch from conventional cotton to lower carbon cotton. Assuming activity data is unchanged, this would be reflected in inventory accounting via a lower emission factor and as lower total emissions.

Under TCAT proposals, an additional effect could also be reported in an Impact Statement as the avoided emissions (the difference in the emissions) that were generated using lower-carbon cotton relative to a baseline of emissions using conventional cotton.

- Decarbonising in the firm’s own sector: captured in a Sector Impact Mitigation Statement

TCAT gives the example of a food and beverage company that sources ingredients from a variety of farms. To support decarbonising the agricultural sector, the company buys carbon credits from a farming cooperative that has obtained emissions reductions from regenerative farming practices. Since the farming cooperative is not part of the company’s supply chain this wouldn’t be reflected in the firm’s usual inventory reporting.

But TCAT proposes that the acquisition of these credits could instead be captured in a Sector Mitigation Statement and be registered as a contribution to decarbonising the agricultural sector - provided the carbon credits are measured, verified and additional.

- Advancing global decarbonisation: captured in a Global Impact Mitigation Statement.

Similarly, TCAT proposes that companies should be able to report and take credit for contributing to decarbonisation outside of their sector. An example would be a firm that acquires carbon credits for a forest planting project despite not having any land-use emissions in its value chain. Crucially, this would not be offset against inventory emissions - keeping the two approaches separate.

Under this multi-statement framework, every activity a company takes to reduce its GHG emissions can be classified into one or more reporting statements. TCAT provides tests and advice for doing so. The guidance has been designed to ensure consistency, avoid double-counting and be externally assurable.

The final result would be a Multi-Statement Report which could look something like the following, reflecting a range of climate impacts achieved by a firm.

The Minimum Line

It’s worth reiterating that the TCAT proposals are just that: proposals. They’re not binding, and no company is being required to produce a Multi-Statement Report, though some are already experimenting with elements of the approach.

The Task Force is currently piloting its framework with several corporate sponsors and expects to release a full consultation early next year. What’s genuinely new is the framing - a formal attempt to elevate impact accounting alongside inventory reporting.

It could prove influential. The GHG Protocol’s work on Actions and Market Instruments has stalled, and TCAT’s proposals give both companies and standard-setters something tangible to calibrate against.

The bigger question is whether this is the right direction. Many companies are still struggling to deliver measurable progress on their own emissions - particularly across scope 3 - and will likely welcome the chance to broaden how success is measured.

But here lies the tension. If impact reporting becomes a substitute for inventory progress, rather than a complement to it, the risk of greenwashing (and over-reliance on carbon credits) increases. TCAT’s approach may expand transparency - or blur it further.