As of March 2026, Minimum.com has been acquired by Novisto - cemeting Novisto’s position as the most comprehensive, "all-in-one" sustainability platform, designed to serve as the single source of truth for global enterprises navigating an increasingly complex regulatory landscape.

The State of Emissions Disclosure in 2025

We take stock of developments in emissions disclosure requirements. The changing political landscape has knocked some of the wind out of the global sustainability agenda. But emissions disclosure requirements remain largely intact and look to be coalescing around IFRS standards.

A quick recap

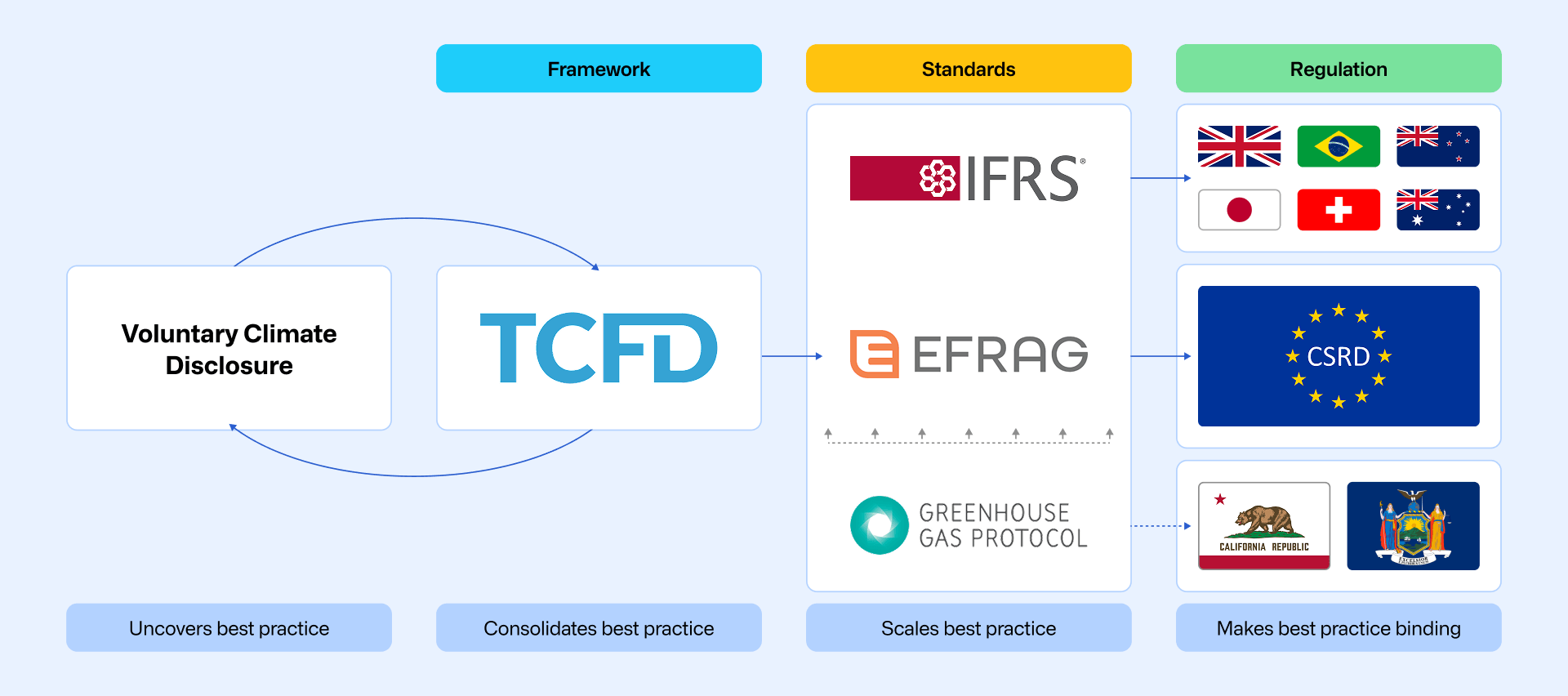

Ten years ago most companies were not calculating or disclosing their emissions.

Things began to change in 2017 with the publishing of the TCFD recommendations, which encouraged firms to report on their climate-related financial risks and opportunities to meet the information needs of capital markets. The recommendations consolidated best practice, including disclosure of scope 1 and 2 emissions, as well as scope 3 if appropriate.

Widespread adoption of the TCFD laid the ground in 2023 for the IFRS Sustainability Disclosure Standards (IFRS SDS) - developed by the IFRS Foundation - which include the climate-specific IFRS S2 standard. As well as the European Sustainability Reporting Standards (ESRS) - published by EFRAG, which contain the climate-specific ESRS E1 standard. These standards translate the TCFD’s high-level recommendations into specific and comparable disclosures.

Over the last few years jurisdictions around the globe have begun to introduce regulation turning recommendations into mandatory requirements. In 2023, the EU approved the Corporate Sustainability Reporting Directive (CSRD) and last year the US SEC brought forward climate disclosure rules. Similar initiatives have been proposed by other jurisdictions.

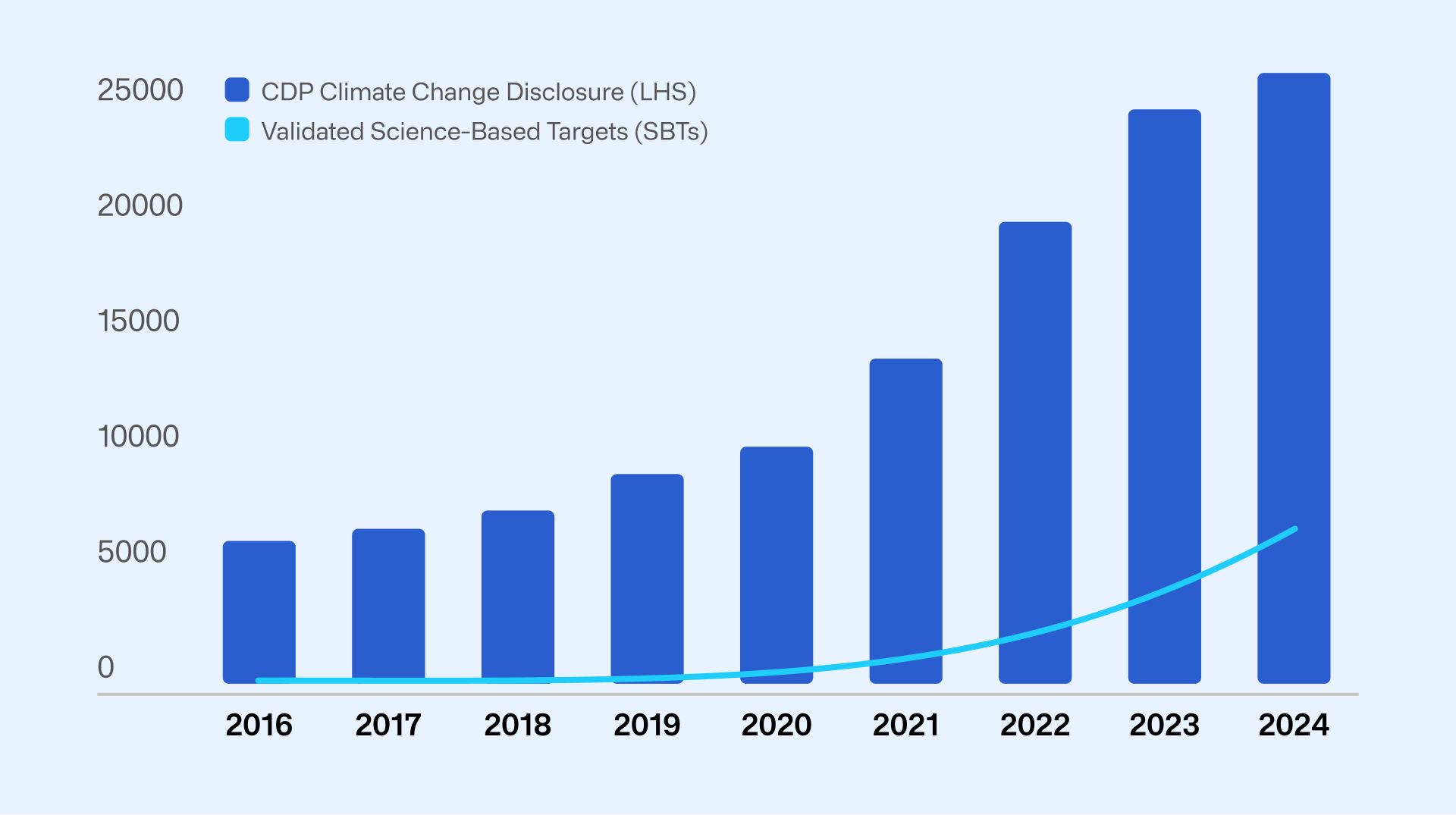

As a result, emissions reporting has become a mainstream activity for large organisations. Nearly 25,000 companies voluntarily disclosed to CDP last year and over 8,000 firms have set validated Science-Based Targets to reduce their emissions.

Two steps forward, one step back

Yet over the last 12 months momentum has begun to falter. A spate of global elections last year returned governments with limited climate ambition or outright scepticism, resulting in a watering down or direct rollback of key aspects of the climate agenda, including disclosure.

For example, in the US, the SEC refused to defend its climate disclosure rules from legal challenges. Meanwhile, the EU introduced the Omnibus I package which simplifies and reduces sustainability reporting burdens.

This has had a knock-on effect on others. Canada adopted a set of standards based on the IFRS but the Canadian Securities Administrators (CSA) decided not to mandate them to “adapt to the recent developments in the U.S. and globally”.

So what is the current state of affairs regarding emissions disclosure requirements?

The state of emissions disclosure requirements

European Union

The ongoing EU Omnibus process will significantly reduce the number of companies in scope of the CSRD and timeframes for implementation will be extended. The EU is also simplifying the ESRS. The goal is to reduce the number of mandatory disclosure points by over 50%.

Given that emissions data is generally considered a highly relevant data point by investors and other stakeholders - to measure a company’s impact on the environment and as an (imperfect) proxy for its exposure to climate risk - it looks likely emissions disclosure will survive the chop.

However, the format of existing requirements could change. In its recent progress report EFRAG noted that it would look to increase interoperability with IFRS standards. This would include eliminating some of the key differences between the two on issues such as reporting boundaries, as well as “adopting the same wording as in IFRS S1 and S2 wherever possible”.

An Exposure Draft of the revised ESRS is due to be published in August.

Global adoption of IFRS Standards

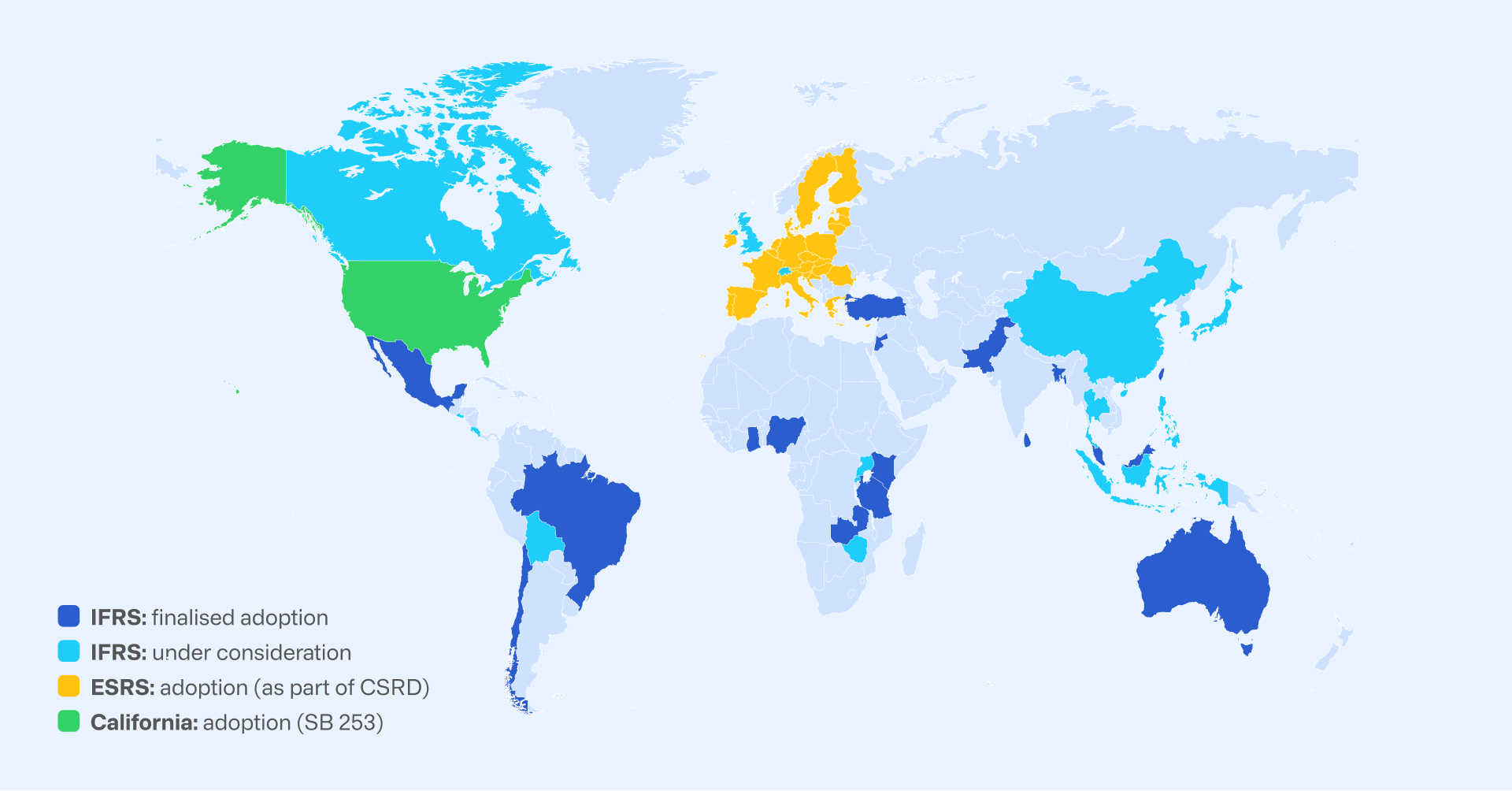

According to the IFRS, thirty-three jurisdictions worldwide have either adopted, committed or are otherwise using the IFRS SDS - either the full set or just the climate-specific elements.

Seventeen jurisdictions have formally announced or finalised decisions on the adoption of IFRS standards. This includes 14 countries that have adopted the full set of standards, two that are in the process of adopting climate requirements, and one that is targeting partial adoption.

A further sixteen jurisdictions are at different stages in the process of reviewing the standards but have yet to finalise adoption. Among this group are large economic powers such as China which has released a draft climate standard modelled after the IFRS and is planning to make disclosure mandatory by 2030.

United Kingdom

Closer to home, last week the UK government released a consultation on draft UK Sustainability Reporting Standards (UK SRS) which are based on the IFRS standards. The UK is proposing minor amendments to the IFRS version. The Financial Conduct Authority will consult on whether to make UK SRS mandatory for listed companies and the government has said it will consider whether to introduce requirements for large private firms to report against the UK SRS.

United States

With the US Securities and Exchange Commission (SEC) refusing to defend its own climate disclosure rules (though the rules are still formally in limbo), the burden of leadership has shifted to individual states.

California set the blueprint with its Climate Corporate Data Accountability Act, which requires US-based companies with over $1bn in revenue, and that do business in the state, to report on their scope 1 and 2 emissions in 2026 and scope 3 in 2027. The rule could impact around 2,000 public and private U.S. based companies.

The California Air Resources Board (CARB) has yet to finalise implementing regulation for the Act but has been urged in consultation responses to align with the IFRS.

State legislatures in several blue states - Colorado, Illinois, New Jersey, New York and Washington - have explored copycat bills, though at the time of writing none have reached fruition

A global baseline

The IFRS’ original intention when developing its sustainability disclosure standards was to create a “global baseline”. And this does now look to be happening - particularly for the IFRS S2 climate standard.

Where once the EU had intended to go further, diminished political ambition in the bloc is leading to a reversion to this baseline.

Another example is last week’s decision by the GRI - as part of its new Climate Change and Energy Standards - to allow companies to “use equivalent disclosures in IFRS S2 on Scope 1, 2 and 3 GHG emissions to meet corresponding requirements in GRI 102”.

It’s important to note that not all jurisdictions that have introduced the IFRS standards are making them mandatory. There are also nuances between countries with regard to in-scope companies and the phasing-in of elements such as scope 3.

Even so, compared to existing voluntary or TCFD-aligned requirements, IFRS S2 represents a step up in several key aspects, including requiring:

- Disaggregation of scope 1 and 2 emissions between the consolidated company-wide footprint and any “off balance” sheet emissions e.g. in JVs

- Detailed information about the measurement approach, inputs and assumptions used in measuring emissions. Such as the consolidation approach and emissions factors.

- A scope 3 measurement framework, which provides guidance on the use of estimates, primary and secondary data, and verified data.

- Specific financed emissions requirements, which are now subject to possible amendment as part of new proposals by the IFRS to ease the burden on companies.

At the end of last month, the IFRS released educational material providing detailed advice on how it recommends companies apply the emissions disclosure requirements.

The Minimum Line

Emissions disclosure has been caught in the political headwinds affecting the sustainability agenda. Fewer companies will be subject to emissions reporting requirements under revised EU rules and rollback in the United States is having contagion effects on other jurisdictions.

However, it has been less impacted than other aspects of the sustainability agenda. For all the politics, users want emissions data from companies to understand how firms are managing their climate-related risks and opportunities and their impact on enterprise value. Good quality data is critical to interpreting how companies are implementing climate initiatives and meeting targets.

And it helps users to make decisions. Whether that’s investors deciding whether to invest (and at what price), lenders looking to determine the cost of lending, or customers determining whether to do business with a company.

While the EU’s Omnibus package continues to stir heated debate as to whether it’s the right response to longstanding competitiveness challenges, or an abdication of sustainability leadership, the global move to align with IFRS standards is good news for companies.

It reduces the need to comply with two sets of slightly differing standards and increases the comparability of disclosures globally.

It also underlines the need for companies to carefully document and understand the assumptions and methodologies underpinning their carbon inventories, as we discussed in our recent webinar on Carbon Inventory Management Plans.